Selling a Cannabis Accounting Firm in 2026: What Buyers Actually Pay For

Cannabis accounting firms trade at 0.9x to 1.35x revenue in 2026. Here's what drives the premium, what kills it, and how to structure the deal.

Selling a firm in this sector requires navigating a valuation landscape distinct from generalist practices. A standard CPA firm trades on retention rates. A cannabis-specific firm gets valued on its mastery of Section 280E, its ability to navigate banking volatility, and its integration with seed-to-sale tracking systems. Buyers are becoming discerning. They aren't just looking for revenue—they're auditing the defensibility of every tax position you've taken for your clients. In an environment where regulatory shifts happen constantly, your firm's intellectual property is its methodology.

This guide is for owners of cannabis-specialized accounting firms looking to exit or merge in 2026. We'll move past generic M&A advice to examine the specific value drivers of this niche: cost accounting for infused product manufacturers, structuring a deal when federal illegality still affects banking covenants, and understanding your worth in this complex market. Whether you're a boutique firm serving local dispensaries or a fractional CFO service for Multi-State Operators (MSOs), your first step toward a successful exit is knowing what you're worth.

The DNA of a Cannabis Accounting Firm: What Buyers Are Really Acquiring

When a buyer evaluates a generalist firm, they look at tax returns and monthly bookkeeping. When they evaluate a cannabis firm, they're looking at a complex ecosystem of cost accounting and regulatory compliance. To maximize your valuation, you have to articulate something simple: you're not a service provider, you're a solution to an existential business problem.

Unlike traditional retail or manufacturing clients, cannabis businesses face a tax code that effectively taxes gross profit rather than net income due to Internal Revenue Code Section 280E. A cannabis accounting firm is defined by its ability to maximize Cost of Goods Sold (COGS) through legal, defensible allocations. Buyers in 2026 are paying premiums for firms that have mastered this.

The Compliance Moat: Section 280E and 471(c)

The most valuable asset in any cannabis accounting practice is your methodology for Section 280E compliance. In 2026, buyers are terrified of inheriting liability. If your firm has been aggressive without documentation, your valuation will suffer. If you've developed proprietary workpapers to allocate labor, overhead, and indirect costs into inventory—and thus COGS—you'll command the highest multiples.

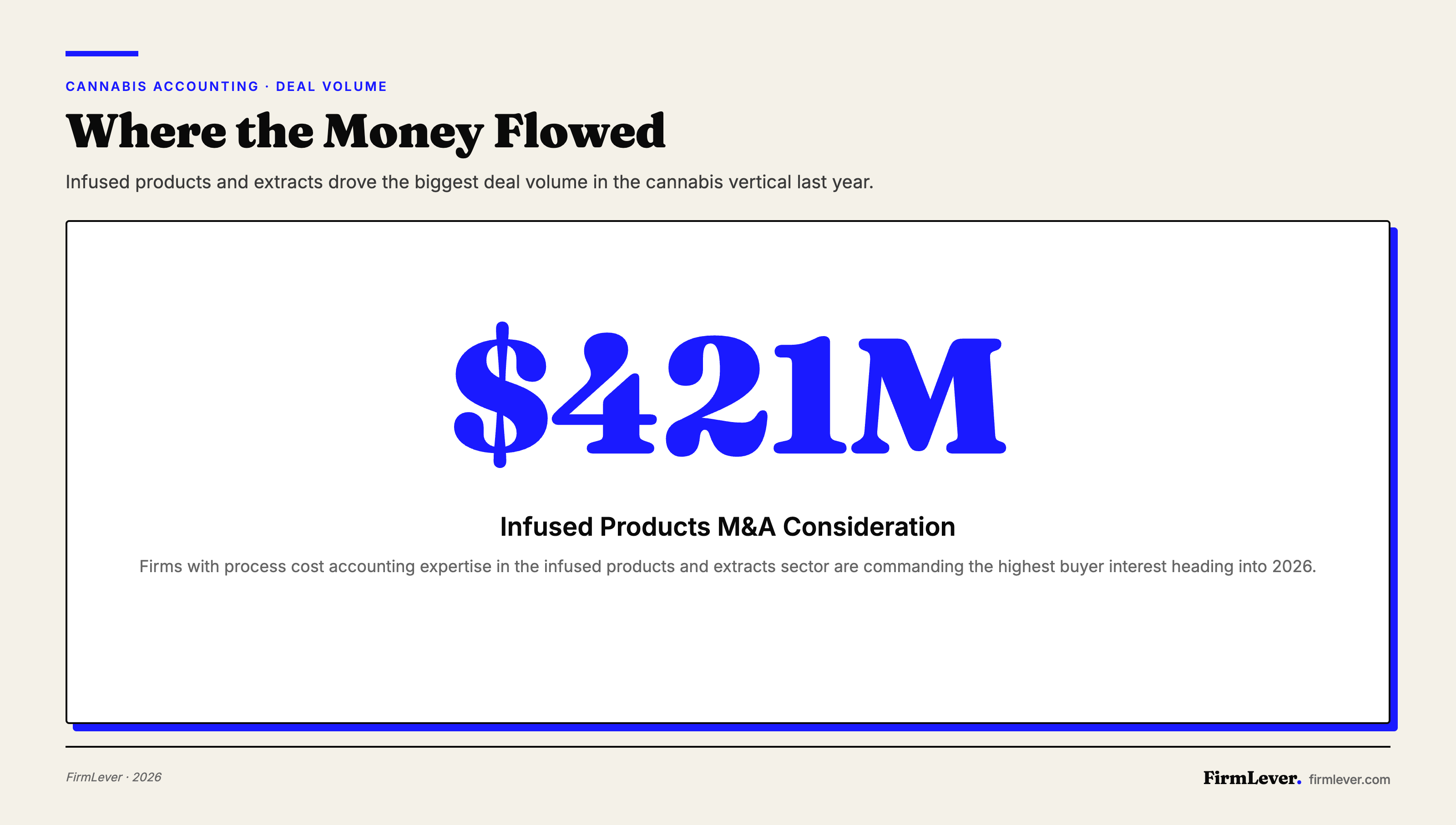

There's high demand for firms that understand the difference between a retailer, who has limited COGS deductions, and a cultivator or processor, who can capitalize significantly more costs. If your firm specializes in the "Infused Products & Extracts" sector, which saw over $421 million in M&A consideration last year, your expertise in process cost accounting is rare.

Beyond the General Ledger: Seed-to-Sale Reconciliation

Cannabis firms have a unique edge: integrating financial data with state-mandated tracking systems like Metrc or BioTrackTHC. Generalist accountants rely on bank feeds. Specialists know that if the inventory in QuickBooks doesn't match the inventory in Metrc, your client is non-compliant.

Buyers look for firms that offer:

- Monthly Inventory Reconciliation: Matching point-of-sale data to the general ledger.

- Unit Cost Analysis: Determining the precise cost to produce a gram of flower or a liter of distillate.

- Excise Tax Management: Navigating the complex web of state and local cultivation and sales taxes.

This operational depth makes client retention sticky, creating the recurring revenue streams that drive valuations toward the 1.35x revenue mark.

2026 Market Dynamics: Valuations and Deal Structures

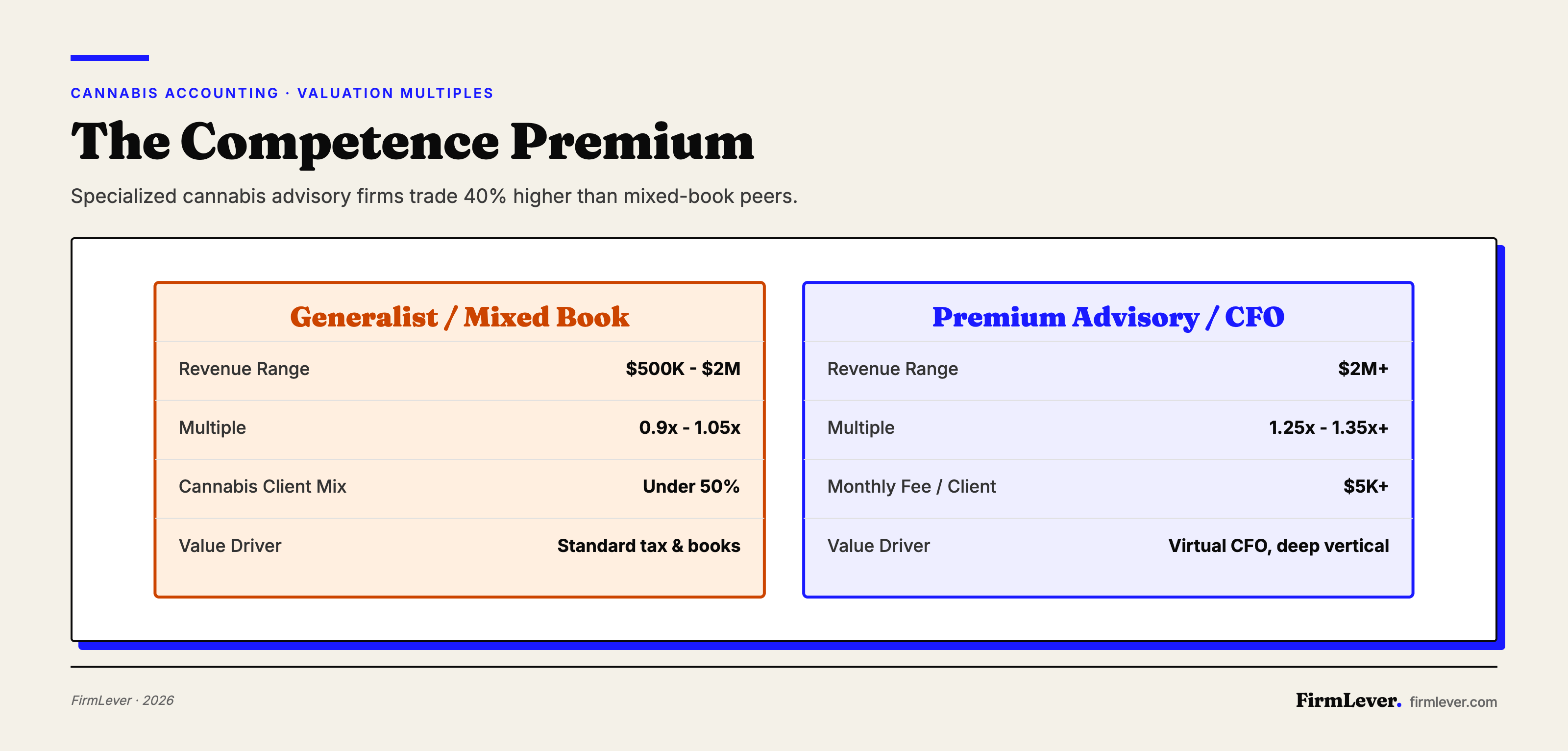

The valuation landscape for cannabis accounting firms has stabilized after the volatility of the early 2020s. The "green premium" has cooled. It's been replaced by a "competence premium." Buyers are paying for proven, specialized cash flow—not hype.

Current Valuation Multiples

Accounting firms in this niche are seeing distinct tiers in valuation:

| Firm Type | Revenue Range | Valuation Multiple | Key Value Drivers |

|---|---|---|---|

| Generalist / Mixed Book | $500K - $2M | 0.9x - 1.05x | Standard tax/bookkeeping, less than 50% cannabis clients. |

| Specialized Compliance | $1M - $5M | 1.1x - 1.25x | Strong COGS methodology, clean audit history, documented SOPs. |

| Premium Advisory / CFO | $2M+ | 1.25x - 1.35x+ | Virtual CFO services, high recurring fees ($5k+/mo per client), deep vertical expertise. |

Cannabis-specific firms face unique downward pressures as well. The "280E discount" is real—buyers will adjust the purchase price based on perceived audit risk. For a broader look at how these metrics stack up against the wider industry, you can refer to The Ultimate Accounting Firm Metrics & Valuation FAQ: 150+ Questions Answered (2026 Edition).

Who are the Buyers?

The buyer pool has shifted in 2026. Fewer individual CPAs are stepping in—they're scared off by the complexity. You're more likely to see:

- Regional Firms Expanding Niches: Mid-sized firms looking to bolt on a high-growth vertical.

- Private Equity-Backed Platforms: Aggregators specifically targeting the cannabis ancillary services market.

- Cannabis Consulting Groups: Legal or operational consulting firms acquiring accounting practices to offer a "one-stop-shop" solution.

For more insights on who is buying in the current market, check out 5 Accounting Firm M&A Predictions for 2026.

Strategic Preparation: How to Position for a Sale

Preparing to sell a cannabis accounting practice requires a different playbook than selling a generalist firm. You're not just cleaning up your own books. You're preparing a defense file for your entire client base.

1. Documentation of Methodologies (The "Playbook")

Document exactly how you handle:

- Cost Allocation: What is your rationale for allocating square footage, electricity, and labor to inventory? Is it based on a time-study? A space analysis?

- Cash Management: Since many clients are still cash-heavy, do you have strict controls to prevent money laundering accusations?

- Software Stack: Document your "tech stack." Firms that successfully integrate tools like Dope CFO, Greenbits, or specialized ERPs are more valuable because the workflow is automated and transferable.

A buyer needs to know that if your lead partner leaves, the methodology remains. This concept is further explored in The Complete Guide to Valuation of Accounting Practice: What Is Your Firm Really Worth in 2026?.

2. De-risking the Client Portfolio

Client concentration is a major issue in this niche. If 40% of your revenue comes from one large Multi-State Operator (MSO), your multiple will plummet. MSOs are notorious for bringing accounting in-house once they reach a certain scale. Diversification is key. A healthy mix of cultivation, retail, and manufacturing clients protects the firm. Also assess the "compliance health" of your clients. If you have clients who refuse to follow your inventory counting protocols, they're a liability. Pruning "risky" clients before a sale can actually increase your firm's value.

3. Financial Clean-Up

Accounting firms often have messy books. For a cannabis firm, you must clearly separate your advisory revenue from your compliance revenue. Advisory revenue (CFO services, cash flow forecasting) is viewed as higher quality and stickier than transactional tax prep. Make sure your own P&L reflects the high-margin nature of your advisory work.

Navigating the Deal: Due Diligence and Structure

Deal structure for selling a cannabis accounting practice often involves a larger earn-out period than standard firms. Why? Because the retention risk is higher. If clients leave because the new owner doesn't understand cannabis, the value evaporates.

The "Cannabis Knowledge" Earn-Out

Buyers will often require the seller to stay on for 12 to 24 months. This isn't just a handshake transition—it's to transfer the technical knowledge of Section 280E and state-specific regulations. Negotiating these terms is critical. Will you be a consultant? A partner? What are the metrics for release?

Addressing Banking and Insurance

Even in 2026, banking remains a hurdle. During the sale, the buyer's bank may balk at financing an acquisition where the underlying revenue comes from cannabis companies. You may need alternative financing or seller financing structures. Professional liability insurance (E&O) for the buyer needs to cover cannabis work. Sorting these logistics early prevents deals from dying at the closing table.

For a deeper look at recent deal hurdles and how other firms are overcoming them, take a look at The Firmlever Weekly Roundup: Issue #31.

The Future: AI and Automation in Cannabis Accounting

The most valuable firms are those leveraging technology to handle compliance. Manual entry of Metrc data is outdated. Firms that use AI to scan invoices and automatically allocate costs to the correct 280E or non-280E categories are commanding premium attention.

Buyers are looking for scalability. If your firm requires one accountant for every five clients, scaling is hard. If your tech stack allows one accountant to handle twenty clients, you have a scalable platform. This efficiency is becoming a primary valuation metric.

Frequently Asked Questions

How does federal rescheduling affect the value of my cannabis accounting firm?

If cannabis is rescheduled (e.g., to Schedule III), Section 280E would likely no longer apply, allowing businesses to deduct standard operating expenses. While this simplifies the tax code, it actually increases the demand for retrospective tax work (amending returns) and strategic business planning. Firms that can pivot from "280E mitigation" to "growth strategy CFO" will see their value increase, while those that only do basic compliance may see fee compression.

Can I sell my firm to a buyer who doesn't have cannabis experience?

It's possible, but difficult. The learning curve for Section 280E and cost accounting is steep. If a generalist buyer acquires a specialist firm, they'll typically require the seller to stay on for a longer transition period (2-3 years) to train staff. The valuation multiple may also be lower to account for the risk of the buyer mishandling the technical work.

How are client contracts handled during a sale?

Most cannabis accounting engagements are at-will, but high-value firms often use engagement letters with 30 or 60-day notice periods. In a sale, buyers will scrutinize these contracts. They prefer "evergreen" engagement letters that automatically renew. For 2026 sales, ensuring your engagement letters have "assignability clauses" (allowing you to transfer the contract to a buyer) is a critical legal step.

What is the biggest deal-killer for cannabis accounting firm sales?

Undocumented aggressive tax positions. If a buyer sees that you've been deducting clearly non-deductible expenses (like marketing or sales staff) for your clients to lower their tax bills, they'll view your client base as a ticking time bomb of audit liability. Conservative, defensible positions are far more valuable in an M&A context.

Should I exclude my 'legacy' clients who pay in cash?

Not necessarily, provided you have strict anti-money laundering (AML) protocols in place. However, buyers generally prefer clients who are banked and pay via ACH or wire. If a significant portion of your revenue is collected in physical cash, it complicates the valuation and the funds transfer during the acquisition. It's advisable to migrate clients to digital payments prior to a sale.

How do I value the "consulting" portion of my revenue vs. the "tax" portion?

Advisory and consulting revenue is generally valued higher because it indicates a deeper relationship and higher margins. When presenting your financials, break out revenue streams distinctly: Recurring CFO Services, Monthly Bookkeeping, Tax Compliance, and One-Time Projects. You can find more on defining these metrics in The Ultimate Glossary of Accounting Firm Metrics, KPIs & Valuation Terms (2026 Edition).

Conclusion

Selling a cannabis accounting practice in 2026 is a sophisticated transaction that involves much more than a simple multiple of revenue. It's a validation of your intellectual property, your risk management frameworks, and your ability to navigate one of the most complex regulatory environments in modern business. The demand is there—driven by firms seeking efficiency and larger players seeking entry into the market—but the scrutiny is intense.

Focus on documenting your compliance methodologies, diversifying your client base, and leveraging technology to automate the unique burdens of cannabis accounting. Position your firm not as a service provider, but as a premium asset. The opportunity is real for firms that have built a solid foundation.

To stay ahead of the curve on valuations, buyer trends, and the shifting landscape of professional services M&A, consider subscribing to our blog for the latest insights.