The CFO's 179D Checklist: Questions to Ask Before Engaging a Specialist

A practical vetting framework for CFOs and controllers evaluating 179D specialists. The right questions to ask about licensing, modeling software, audit defense, and fees before signing an engagement letter.

What is a 179D specialist, and why vet one carefully?

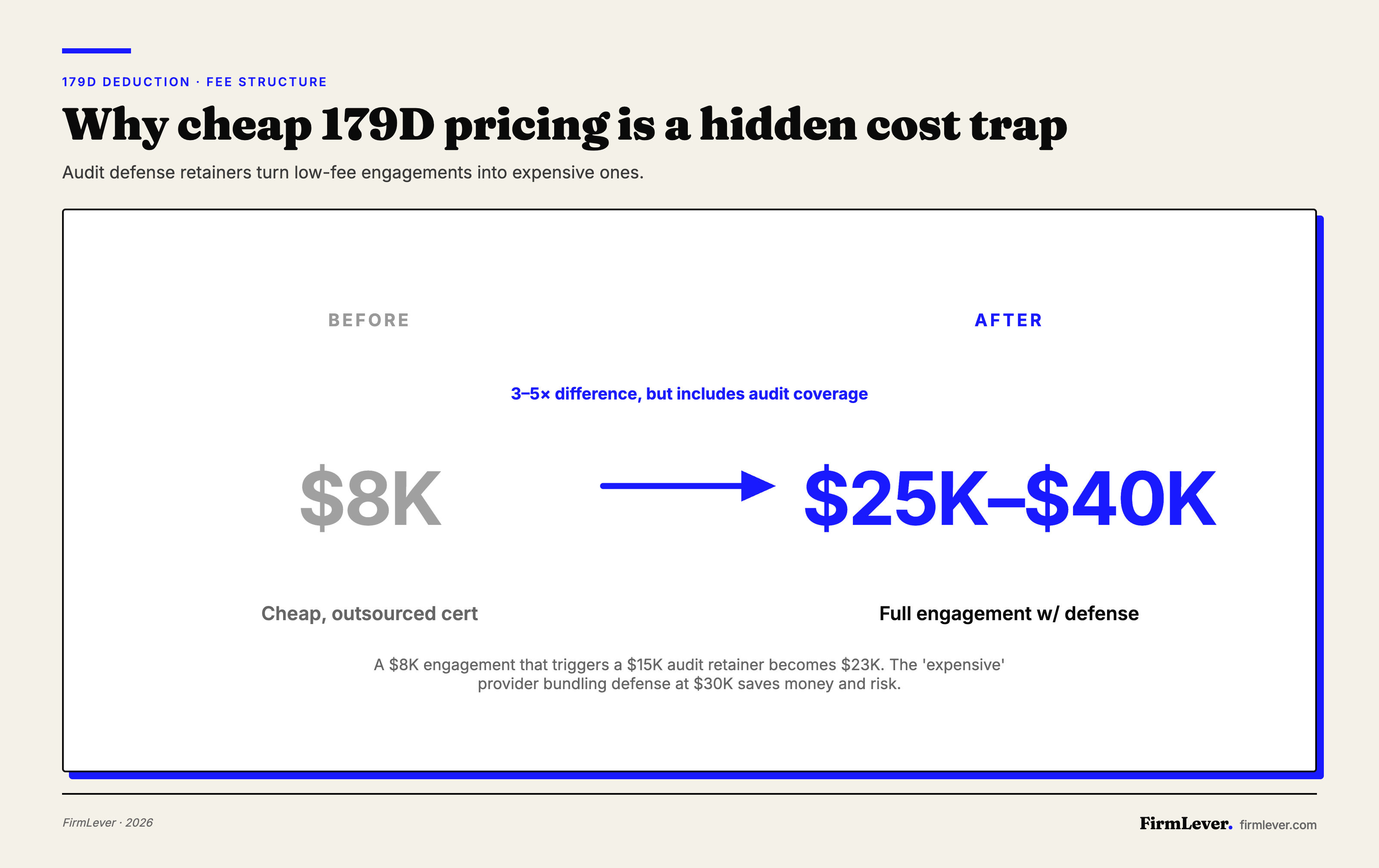

A 179D specialist is a firm that performs the energy modeling, site verification, and professional engineer certification required to claim the Section 179D Energy Efficient Commercial Building Deduction. Fees range from $8K–$40K per engagement depending on scope. Because the deduction requires a licensed PE or registered architect to certify the energy model, and because the IRS scrutinizes these claims closely, choosing the wrong provider can mean the difference between a clean deduction and an audit-driven clawback with penalties.

Section 179D allows owners of commercial buildings, and the designers of government or tax-exempt buildings, to deduct up to $5.81 per square foot (2024 figure, adjusted annually) for qualifying energy-efficient improvements to HVAC, lighting, and building envelope systems. The deduction was made permanent and expanded under the Inflation Reduction Act, which raised both the potential benefit and the technical bar for qualification. This shift has driven more 179D provider pitches in recent years, and CFOs need to distinguish between firms with genuine engineering capability and those reselling outsourced work.

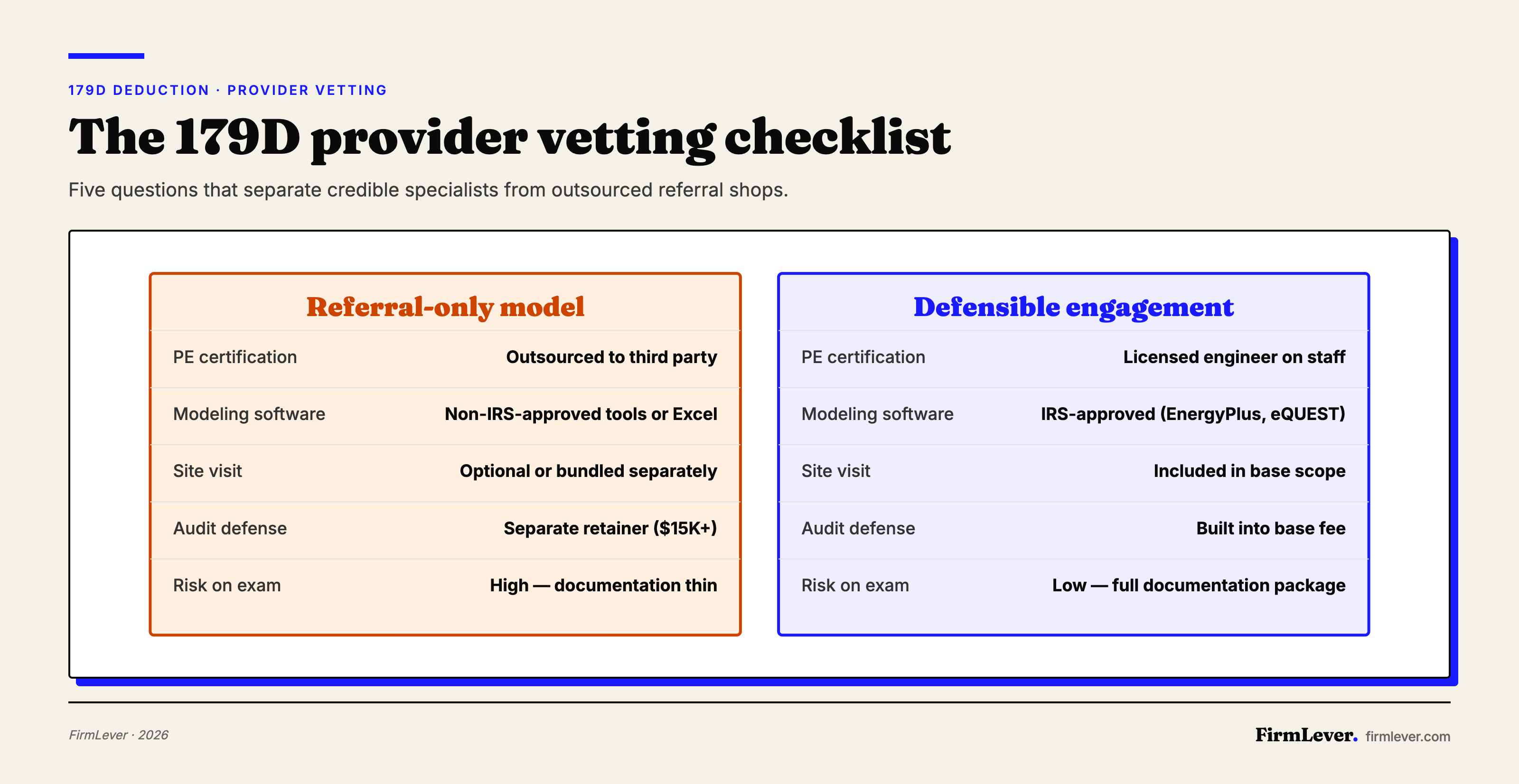

This checklist is built for CFOs, controllers, and tax directors who have already identified a potential 179D opportunity and are now evaluating two or three providers. The goal is to separate firms with real engineering depth from those running a referral-only model with outsourced modeling.

Credentials and licensing questions

The first category of questions goes to whether the firm can legally and defensibly perform the work. 179D certification requires a licensed professional engineer or registered architect who is independent of the taxpayer. That independence requirement alone disqualifies the taxpayer's own design-build contractor or in-house engineering team from signing the certification.

Ask the provider directly:

- Does the firm employ licensed PEs or RAs on staff, or does it subcontract certifications to a third party? In-house licensure is preferable.

- In which states is the certifying engineer licensed? 179D requires licensure in the state where the building is located.

- How many 179D certifications has the lead engineer personally signed in the past two years? Fewer than a dozen is a yellow flag for a firm marketing itself as a specialist.

- Is the firm carrying professional liability insurance that specifically covers tax certification work? Generic E&O policies sometimes exclude it.

If a provider cannot answer these in the first call without checking with someone else, the engagement is likely being run by a sales team rather than a technical team. CFOs should also confirm that the PE signing the certification will be identifiable on the final deliverable, not masked behind the firm's brand.

Modeling software and methodology questions

The energy model is central to a 179D study. The IRS requires modeling performed in software on its approved list, which is periodically updated and currently includes tools such as EnergyPlus, eQUEST, and certain commercial derivatives. Any provider claiming to perform 179D work in Excel or in a proprietary tool not on the IRS list is not doing defensible 179D work.

Questions to raise:

- Which IRS-approved modeling software does the firm use, and is it operated in-house?

- How is the ASHRAE 90.1 reference building constructed, and which version of the standard is being applied? The IRA shifted the reference to ASHRAE 90.1-2007 for most buildings, with later standards applying as they're adopted.

- Is a site visit included in the base scope? For new construction, the certifier must verify as-built conditions. For retroactive studies, documentation review and site inspection together form the audit trail.

- How are partial qualifications handled if the building meets the threshold on lighting but not HVAC?

The answers reveal whether the firm understands the mechanics or is running a templated process. A provider who understands the ASHRAE baseline, the whole-building performance path, and the interim lighting rules legacy path is demonstrating the depth required for defensible work.

Fee structure questions

179D fees vary widely, and the structure matters as much as the number. Fixed fees or tiered fees based on square footage and building count are the norm for defensible engagements. Contingency pricing, where the provider charges a percentage of the deduction claimed, exists in the market but raises concerns under Circular 230.

CFOs should ask:

- Is the fee fixed, tiered, or contingent on the deduction amount?

- What is included in the base fee versus billed as extras? Common add-ons include additional site visits, modeling for complex mechanical systems, and amended return support.

- Does the engagement include the final certification letter, the supporting energy model, and the as-built documentation package? All three should be deliverables.

- Is audit defense included, and if so, what does it cover?

Audit defense is often the most underweighted line item in the 179D vetting process. A study that looks cheap on paper but carries a separate $15K retainer for audit support ends up costing more than a higher-fee engagement with defense built in. Most credible 179D providers now bundle a defined scope of audit support into the base fee, typically covering the first round of IRS inquiry and supporting documentation requests.

Documentation and audit defense questions

Even a perfectly executed 179D study can be selected for IRS examination. The quality of the documentation package determines whether that examination is quick or prolonged. The 179D deduction has historically appeared on IRS compliance focus lists, particularly for designers of government buildings, so the documentation bar should be treated as audit-ready from day one.

Key questions:

- What documents are delivered at engagement close? A defensible package includes the signed certification letter, the full energy model file, the ASHRAE baseline documentation, site visit photos and notes, construction drawings reviewed, equipment cutsheets, and the allocation letter from the government entity if applicable.

- Who retains the working files if the firm is acquired or ceases operations? The client should have archival copies, not just access through a vendor portal.

- What is the firm's track record on IRS exams? Reputable providers will share anonymized exam statistics readily.

- How quickly can the firm respond to an IDR (information document request) if one arrives three years post-engagement?

For designers claiming 179D on government or tax-exempt buildings, the allocation letter from the building owner is a specific point of failure. The provider should have a standard allocation letter template and direct experience securing these from state agencies, school districts, and federal entities, each of which has different internal processes.

Industry and project-type fit

179D qualification mechanics differ by building type. A cold-storage warehouse, a Class A office tower, a public school, and a multifamily building placed in service after 2023 all raise different modeling and allocation issues. A provider whose portfolio is mostly office buildings may struggle with a refrigerated distribution center or a hospital.

Skip the vetting — get intro'd to our 179D Energy Efficient Commercial Building Deduction specialist.

FirmLever has vetted a 179D Energy Efficient Commercial Building Deduction specialist for exactly this kind of engagement. Tell us about your situation and we'll make the intro — usually within one business day. No cost.

Request a match →CFOs should ask for:

- A list of comparable projects by building type and square footage in the past 24 months.

- References from two or three clients in a similar vertical, including at least one where an IRS inquiry occurred.

- Whether the firm has experience with the prevailing wage and apprenticeship requirements that apply to buildings placed in service after January 1, 2023. These requirements significantly affect the per-square-foot deduction rate and require specific documentation the provider must help the client assemble.

For architecture and engineering firms pursuing designer 179D allocations on government buildings, another question: does the provider have established intake relationships with state and municipal entities, or will the A&E firm be responsible for securing allocation letters? This operational detail can determine whether a deduction gets claimed in the current tax year or slips to the next.

Red flags to screen for

A few patterns recur across failed 179D engagements:

- Contingency-only fee pitches with no fixed-fee alternative offered. This often indicates the firm is optimizing for volume over defensibility.

- Promises of qualification before a feasibility review. No credible provider guarantees an outcome before seeing construction documents and running a preliminary model.

- Outsourced PE certifications where the signing engineer has no direct involvement in the modeling or site visit. The IRS has begun scrutinizing pass-through certification arrangements.

- Marketing that emphasizes deduction size over documentation quality. A $2 million deduction that gets clawed back is worth less than a $1.4 million deduction that survives exam.

- Reluctance to provide references or exam history. Legitimate specialists provide both on request.

Next steps

The questions above form a screening framework, not a full due diligence process. A complete vetting typically involves two or three provider calls, a reference check, and a review of a sample deliverable package before signing any engagement letter. For CFOs evaluating a 179D opportunity for the first time, a no-cost feasibility review on a single candidate building is a useful first move. That narrow engagement reveals more about a provider's technical depth and responsiveness than any sales pitch.

Frequently asked questions

Can our existing CPA handle a 179D study?

Generally no. Section 179D requires an energy model certified by a licensed professional engineer or registered architect who is independent of the taxpayer and the design team. Most CPA firms don't have PE licensure in-house and will either refer the engineering portion to a specialist or decline the work entirely. The CPA can still handle the tax return filing, but the certification itself must come from a qualified third party.

What's the difference between a 179D specialist and a cost segregation firm?

They're adjacent but distinct. Cost segregation reclassifies building components into shorter depreciation lives. 179D certifies energy-efficient improvements to qualify for a per-square-foot deduction. Some firms offer both services, which can be efficient if a single building qualifies for both analyses. However, the 179D work specifically requires PE-stamped energy modeling, which not every cost seg firm performs in-house.

How long does a 179D study typically take?

Most engagements run 6 to 12 weeks from kickoff to final certification package. The timeline depends on how quickly the client can produce construction drawings, specifications, and equipment cutsheets, and whether a site visit is required. Retroactive studies on older buildings often take longer because documentation has to be reconstructed. Providers who promise 2-week turnarounds are usually cutting corners on the modeling or site verification.

Is contingency pricing allowed for 179D work?

It's a regulatory gray area. Circular 230 restricts contingent fees for services that involve taking a position on a tax return, and many tax advisors interpret this to exclude percentage-of-deduction pricing for 179D. Some firms structure contingency arrangements around the engineering study itself rather than the tax outcome. CFOs should ask the provider to explain their fee structure in writing and confirm it has been reviewed by counsel.

What happens if the building doesn't qualify?

A qualified specialist should perform a no-cost or low-cost preliminary feasibility review before accepting the engagement. If the building fails to meet the energy reduction thresholds, the study doesn't proceed to certification and no deduction is claimed. Some firms charge a nominal fee for the feasibility work; others absorb it. Either way, the CFO should never be surprised by a full invoice on a building that couldn't qualify in the first place.

Do we need a site visit for every building?

For most 179D claims, yes. The IRS expects the certifying engineer to physically inspect the building to verify that the as-built conditions match the construction documents. Exceptions exist for certain retroactive studies where the building is no longer accessible, but those require additional documentation to defend. A provider who skips site visits entirely as standard practice is creating audit exposure for the client.

How far back can we claim 179D?

Buildings placed in service going back several years can still qualify, though the mechanics vary. For buildings in open tax years, the deduction can typically be claimed on an amended return. For closed years, a Form 3115 change in accounting method is generally required to pick up the missed deduction in the current year. The specialist and CPA should coordinate on which approach applies to each property.

Get matched

Need a 179D Energy Efficient Commercial Building Deduction specialist for your situation?

FirmLever's 179D Energy Efficient Commercial Building Deduction specialist handles this exact kind of work. Share a few details about your deal or engagement and we'll make the introduction — typically within one business day. No obligation.

Request a specialist match →