Buying a Cannabis Accounting Firm in 2026: The 280E Moat Play

Cannabis accounting firms trade at 1.35x revenue in 2026. Here's how to value the 280E moat, spot red flags, and structure the earn-out.

The market has shifted hard over the last twelve months. Speculative growth is over. What's left is a focus on profitability and consolidation. Generalist firms are struggling to hold margins while specialized cannabis practices are commanding premium valuations because clients can't afford to switch. If you're considering an acquisition in this space, you're not just buying revenue. You're buying regulatory knowledge that protects clients from existential threats like Section 280E. The question is how to value a firm operating in a federally gray area, and how to tell a gold-standard practice from a compliance liability.

This requires a departure from the standard M&A playbook. Retention rates and basic EBITDA tell only half the story. Below I'll walk through what actually separates a high-value cannabis accounting firm from a generalist, the valuation multiples I'm seeing in 2026, and a due diligence roadmap that gets at the real quality of a firm's expertise.

The state of the market: consolidation and specialization

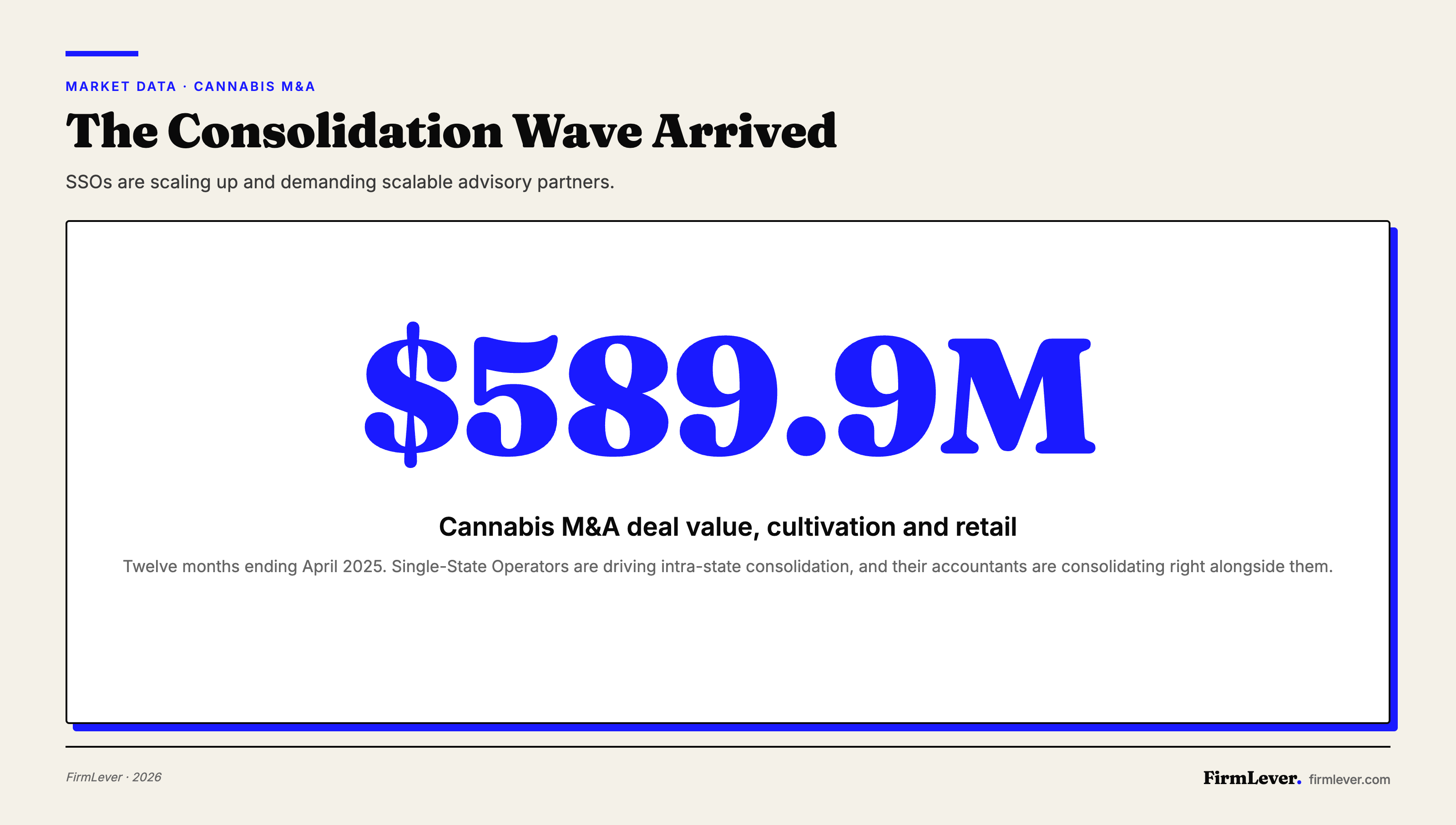

The consolidation wave people predicted a few years ago is here. In the 12 months ending April 2025, the cultivation and retail sectors alone saw $589.9 million in M&A deal consideration. Most of this is Single-State Operators (SSOs) doing intra-state consolidations to get scale and efficiency before attempting multi-state expansion.

For accounting firms, this creates a split market. Small operators are exiting or merging. The ones left are getting bigger, more complex, and desperately need fractional CFO services and sophisticated tax planning. Service providers that can scale with consolidating SSOs are seeing their own valuations rise.

The 2026 outlook hints at regulatory clarity, possibly through federal rescheduling or banking reform. But until full legalization happens, banking friction and 280E are the two things driving value for accounting firms. M&A in Infused Products & Extracts ($421.1M) and Real Estate ($58.9M via sale-leasebacks) shows the industry is diversifying. A firm that actually understands extraction manufacturing versus simple retail is worth a premium.

What actually makes a specialized cannabis firm specialized

When you set out to buy a cannabis accounting firm, you have to tell the difference between a firm that "accepts cannabis clients" and one that "specializes in cannabis accounting." That's not semantics. One is a liability, one is a gold mine.

1. Section 280E and COGS allocation

Section 280E is the whole game. It prohibits businesses trafficking in Schedule I or II controlled substances from deducting ordinary business expenses, except for Cost of Goods Sold. A generalist files a standard return and the client ends up with an effective tax rate of 70% or more. A specialist knows how to maximize COGS allocations aggressively while staying defensible.

When you're vetting a target firm, look at how they handle:

- Inventory accounting (IRC 471): Are they using proper absorption costing? A specialist capitalizes labor, overhead, and indirect costs into inventory, pushing them above the line to reduce taxable income.

- Entity structuring: Good firms help clients stand up separate entities for non-plant-touching activities like branding or management to isolate 280E exposure. This has to be done carefully to survive an audit.

2. Seed-to-sale tracking reconciliation

In cannabis, inventory management is compliance management. States use track-and-trace systems like Metrc or BioTrack to monitor every gram of biomass. A real specialist doesn't just trust the client's POS. They reconcile financials against the state compliance system.

Does the firm you're looking at offer monthly health checks between the general ledger (QBO or Xero) and the state tracking system? If not, the client's inventory numbers are almost certainly wrong and the tax liability is miscalculated. This reconciliation work is high-value recurring revenue and it's one of the clearest tells of genuine expertise.

3. Banking and cash management compliance

Banking is still a hurdle. Specialist firms often offer Bank Secrecy Act (BSA) readiness services, preparing the documentation banks demand to open and maintain cannabis accounts. That includes precise cash handling logs and Form 8300 compliance for cash payments over $10,000. If the target firm runs this as a managed service, client stickiness jumps.

Valuation multiples: what is a firm worth in 2026?

Valuing a cannabis accounting firm means recalibrating on risk and reward. Mid-sized accounting firms in the broader market ($500K-$2M revenue) are trading at 0.9x to 1.2x revenue. Premium cannabis firms with recurring advisory revenue are hitting 1.1x to 1.35x.

Why the premium? The moat. 280E and state-by-state rules create a brutal barrier to entry. Clients are genuinely scared to switch accountants because one mistake can mean bankruptcy. That produces churn rates competent firms in other niches can only dream about.

Adjusting for risk

Multiples are high, but EBITDA calculations get messy. MSO median EV/EBITDA multiples were hovering around 5.2x in May 2025, jumping to nearly 6.5x once adjusted for tax liabilities. The same logic applies when you're valuing a firm that serves this sector. You have to adjust for the volatility of the client base.

For how to actually run these calculations, see The Complete Guide to Valuation of Accounting Practice: What Is Your Firm Really Worth in 2026?. You'll probably need to normalize earnings for the higher professional liability insurance costs and the ongoing staff training needed to keep up with rule changes.

Due diligence: red flags and value drivers

Once you're ready to make an offer, diligence has to go past the financials. You're buying the firm's ability to keep clients compliant. Here's what to scrutinize.

1. Client concentration and licensure status

Some firms still service unlicensed gray market operators. In 2026, that's a deal-breaker. Verify 100% of the firm's revenue comes from state-licensed operators. Then look at concentration. If 40% of revenue comes from two large cultivators and those cultivators are in a state hit by oversupply and price compression, the firm's revenue is at risk.

2. Tech stack integration

Is the firm relying on manual entry, or have they automated the flow from cannabis-specific ERPs (like MJ Platform or Treez) into the accounting software? Firms that have built proprietary connectors or workflows to handle the data volume of cannabis retail have a real competitive advantage.

For more on how tech affects firm value, see The Ultimate Accounting Firm Metrics & Valuation FAQ: 150+ Questions Answered (2026 Edition).

3. Staff expertise vs. partner knowledge

Is the knowledge written down, or does it live in the seller's head? Cannabis accounting is full of nuance. If the seller is the only person who knows how to allocate facility costs between grow (COGS deductible) and retail (non-deductible), the firm has no transferable value. Look for documented SOPs specifically covering 280E allocations.

Deal structure and integration

Because of regulatory volatility, deal structures in this niche lean heavily on earn-outs. A typical 2026 structure is 60% cash at close with 40% tied to a two-year retention and revenue growth target. That protects the buyer if federal rescheduling or some other big change wipes out the complexity (and the pricing power) of the services.

That said, federal rescheduling could also be a huge tailwind. If cannabis gets rescheduled and 280E goes away, demand for cleanup work and transition advisory will spike. That lines up with 5 Accounting Firm M&A Predictions for 2026, where we argued regulatory shifts usually precede M&A booms.

The integration challenge

Culture will make or break this. Cannabis clients expect their accountants to be responsive, tech-savvy, and genuinely sympathetic to how stressful the industry is. Merging a laid-back traditional firm with a high-octane cannabis practice can be a disaster if you don't manage expectations on both sides.

| Feature | Generalist Firm | Specialist Cannabis Firm |

|---|---|---|

| Tax Strategy | Standard Deductions | Aggressive COGS / 280E Mitigation |

| Inventory | Periodic Counts | Perpetual / Seed-to-Sale Reconciliation |

| Audit Risk | High (due to misclassification) | Low (defense-ready documentation) |

| Pricing Model | Hourly / Annual | Value-Based / Monthly Subscription |

Frequently asked questions

1. Is it legal to buy a cannabis accounting firm given federal prohibition?

Yes. Providing accounting and tax services to cannabis companies operating legally under state law is generally low risk for prosecution, and most state boards of accountancy have issued guidance allowing it. Buyers should still check with legal counsel about banking covenants and insurance policies that may restrict cannabis-related revenue.

2. How does Section 280E impact the valuation of the accounting firm itself?

Indirectly, through the health of the client base. 280E compresses client margins, which can mean cash flow problems for clients and bad debt for the firm. But the complexity of 280E is also what lets the firm charge higher fees. A firm that handles 280E well is worth more than one that doesn't.

3. What happens to these firms if cannabis is federally legalized?

If cannabis gets fully legalized and descheduled, 280E goes away. Some people worry that kills the need for specialists, but the industry would immediately face new complexity — federal excise taxes, FDA-style regulation. Demand for advisory services shifts rather than disappears.

4. What are the key metrics to track post-acquisition?

Beyond standard KPIs, track Compliance Score (accuracy of client state reporting) and Revenue per Client (which should be well above the industry average). For a full list, see The Ultimate Glossary of Accounting Firm Metrics, KPIs & Valuation Terms (2026 Edition).

5. Can I use SBA financing to buy a cannabis accounting firm?

It's a gray area. The SBA generally restricts loans to businesses with direct cannabis involvement (plant-touching). Indirect businesses like accounting firms are usually eligible as long as they don't derive revenue from the sale of cannabis itself. Underwriting is strict and plenty of lenders still won't touch it. Private or seller financing is often more reliable in this niche.

6. How do I verify the quality of a firm's "Cannabis CFO" services?

Ask to see redacted monthly reporting packages. Real CFO work includes metrics like Cost per Gram, Yield per Square Foot, and Labor as % of Revenue. If the reporting is just a P&L and balance sheet, it's not CFO advisory.

7. What is the typical churn rate for cannabis accounting clients?

For specialist firms, churn should be very low — under 5%. It usually only happens when a client goes out of business or gets acquired. Voluntary churn above that is a red flag pointing to weak service or technical gaps.

Conclusion

Buying a cannabis accounting firm in 2026 is a bet on high-margin, sticky revenue in a sector that's still sorting itself out. The buyers who do well here are the ones who look past the hype and focus on the technical rigor of the practice. Validate the firm's handle on 280E, check that the tech stack actually talks to state compliance systems, and structure the deal to account for regulatory volatility.

As the market consolidates, the window to pick up premier boutique firms at reasonable multiples is narrowing. The firms that can handle both strict compliance and strategic growth are the ones I'd be trying to buy right now.

To keep up with valuations, deal structures, and what's happening in professional services M&A, subscribe to the blog. I send the latest insights straight to your inbox to help you make smarter acquisition calls in a complicated market.