Accounting Firm Client Concentration Risk: The Three Thresholds That Decide Your Multiple

Client concentration is the single biggest reason buyers chop a firm's valuation. Three thresholds decide whether your book trades at a premium or a discount.

Bigger isn't always better--especially when it comes to clients.

Accounting firm client concentration risk is the financial and operational exposure a firm carries when too much of its revenue depends on too few clients.

The hard numbers: no single client should exceed 15% of revenue, the top 10 clients combined should not exceed 40%, and the aspirational target is no client above 5%. Cross those lines and your firm becomes harder to sell, harder to finance, and harder to staff through a downturn.

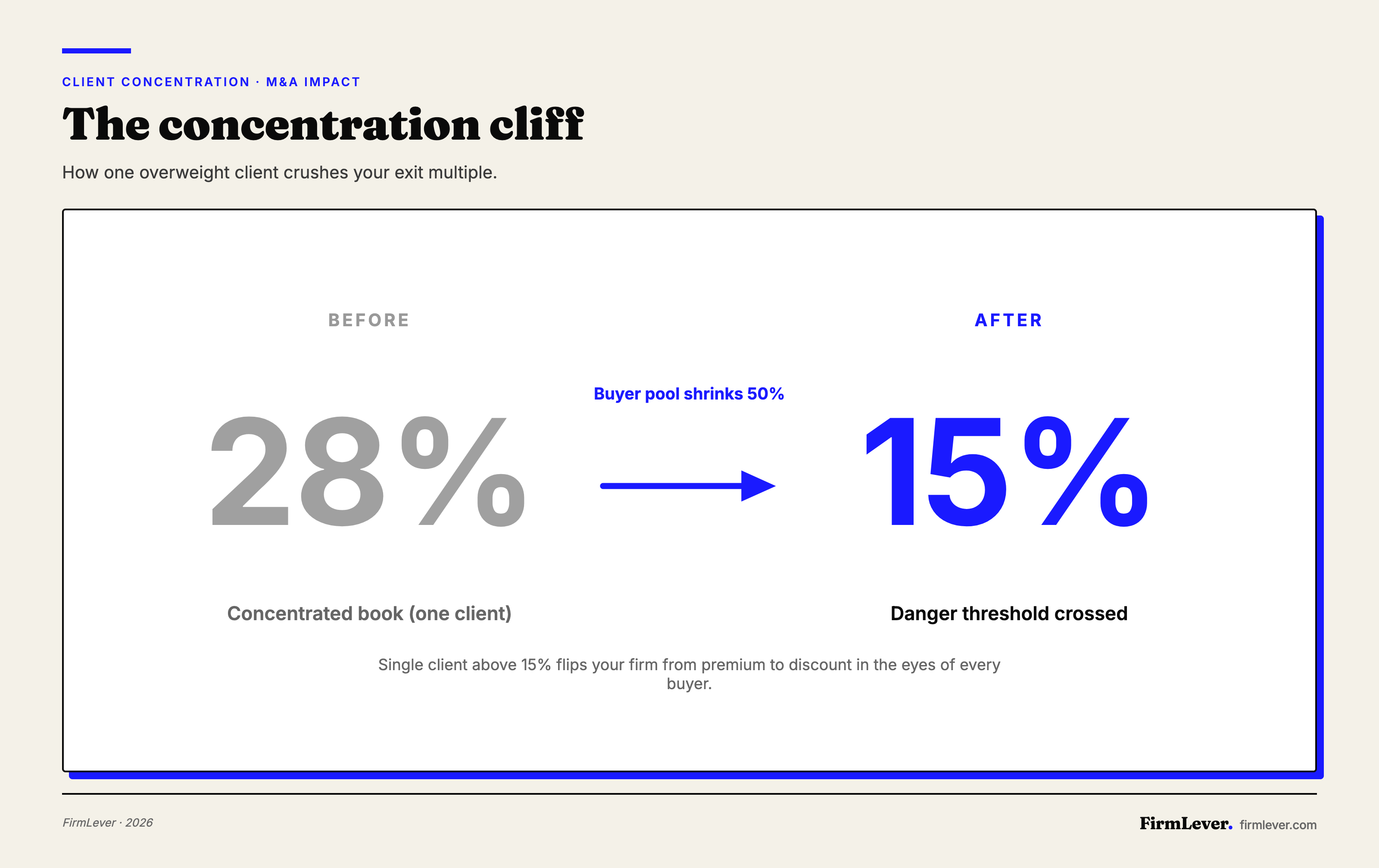

I see this every week on FirmLever. A founder lists a $1.8M book. Looks great on the surface. Then the data room opens and one client is 28% of revenue. The buyer pool shrinks by half overnight. The ones who stay want a longer earn-out and a smaller check at closing.

Concentration is the single biggest unforced error in this industry.

The three thresholds, and why each one matters

The 15% rule (single client cap). No individual client should be more than 15% of your revenue. This is the danger line. Above 15%, the loss of one relationship creates an immediate margin crisis. Buyers know it. Lenders know it. Insurance underwriters know it.

The 40% rule (top 10 combined cap). Your ten largest clients combined should not exceed 40% of revenue. This catches the firm that has no single 15% client but has eight clients at 8% each. A buyer looks at the top 10 list and asks: if half of these walked, can the firm survive? At 40% combined, the answer is yes. At 65%, it is not.

The 5% rule (aspirational target). The best books have no client over 5%. That is the standard you aim for.

If you only remember one number, remember 15. That is the line that flips your firm from premium to discount.

What concentration actually costs you at sale

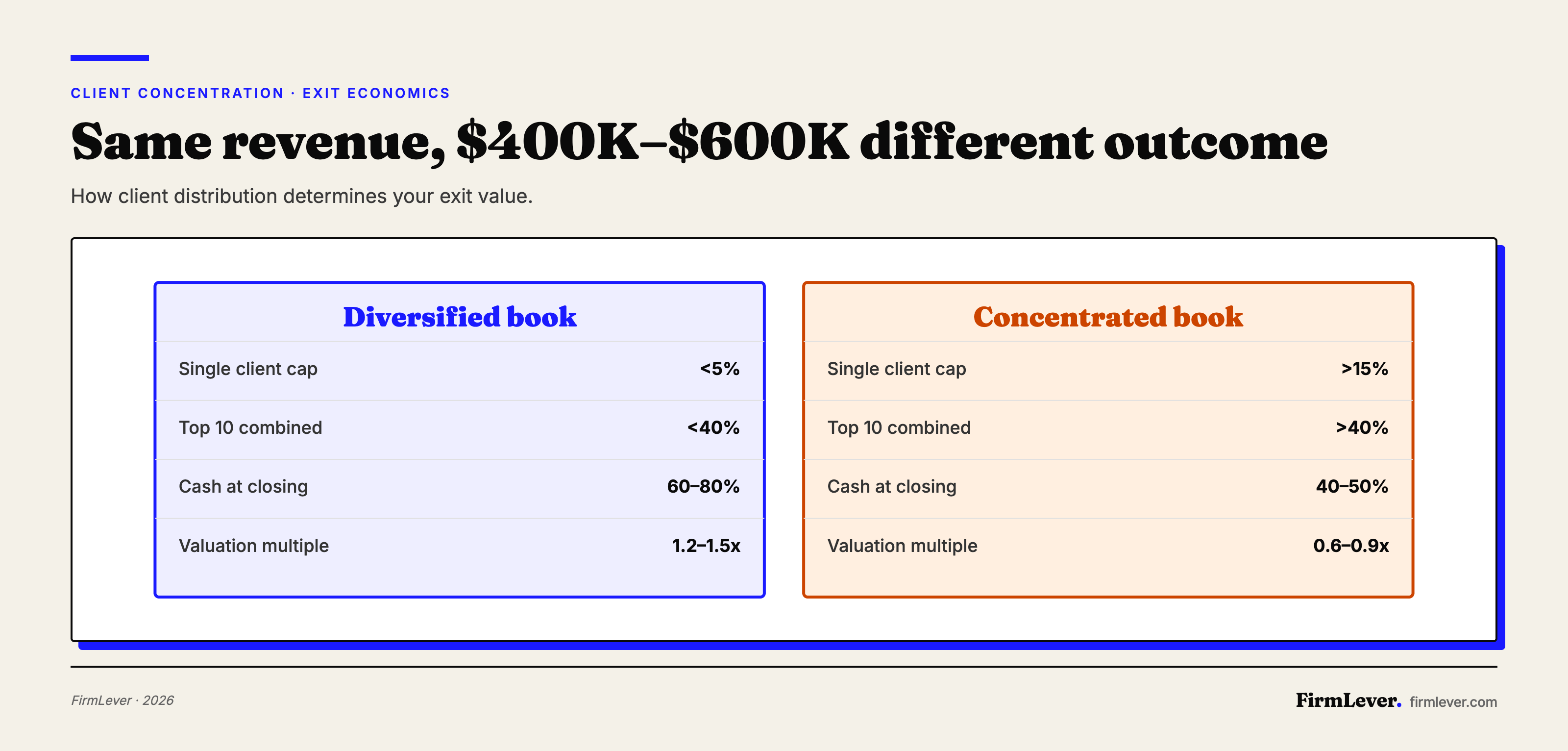

A clean, diversified book sells at 60% to 80% cash at closing. A concentrated book with realization issues or partner dependency sells at 40% to 50% cash with two to three year earn-outs for the balance. On a $2M sale, that is $400K to $600K of cash you do not get on day one.

The multiple moves too. Team-centric, systematized firms trade at 1.2x to 1.5x revenue. Partner-dependent firms with concentration trade at 0.6x to 0.9x. Same revenue, different outcomes, all because of how the client mix is distributed.

Concentration almost always travels with partner dependency. The 28% client is usually the founder's golfing buddy from 1998. The buyer is not buying that relationship. The buyer is buying a risk that walks out the door the day the founder retires.

How concentration actually happens

You land a great client in year three. They grow. You grow with them. They refer two of their portfolio companies. Now you have three related clients that look like three logos but behave like one decision-maker. Five years in, that "client family" is 35% of your revenue.

Or you build a niche, and then you let the niche become two or three whales. Specialization with three clients is the problem. Specialization with thirty clients is the moat.

The firms that stay diversified do it on purpose. They turn down work. They cap individual clients at a known percentage. They refer the overflow out, often to peers in a network, instead of taking it and getting more concentrated.

The fix, by quarter

This quarter: Run the report. Top client as a percent of revenue. Top 10 as a percent of revenue. Identify every "client family" where related entities share a decision-maker and treat them as one client for this analysis.

Next quarter: Stop adding to the problem. If your top client is at 22%, you do not get to take more work from them. Their growth from here goes to a peer. You can still serve them well. You just stop deepening the dependency.

Within the year: Add diversifying revenue faster than you add concentrated revenue. This is where a referral network matters. Inbound work from peers, in your niche, sized appropriately, dilutes the percentage without forcing you to fire your biggest client.

Within two years: If a single client is still over 20%, consider a structured handoff. Sometimes the right move is to refer that client to a firm built to serve them, take a referral fee, and rebuild the slot with three smaller engagements. Worth 0.4x of multiple at exit.

Why this matters more in 2026

AI is compressing the value of commodity work and expanding the premium on judgment and niche expertise. The firms winning right now are specialists. But specialization done wrong creates concentration, and concentration kills the multiple that specialization is supposed to earn.

Be deep in a niche and wide in your client base inside that niche. Thirty manufacturing clients beats three. Forty dental practices beats four. Same expertise, different risk profile, completely different valuation.

Marc

P.S. — FirmLever is where firms with concentration problems trade their way to a cleaner book. Members refer overflow work, list slices of their book to peers who can absorb it, and pull diversifying engagements from a network of 316 vetted firms across 43 states. If your top client is sitting above 15% and you want options that are not "wait and hope," the network is open.